Dear readers,

The world seems to be going through yet another convulsion. I have pushed to get this piece of writing out as soon as I could in anticipation of the upcoming meeting next week of the SBP’s monetary policy committee. My analysis could very well turn out to be wrong, but I wanted it to be on the record before the meeting. There seem to be perilous waters ahead for us all. I hope you keep well.

Sincerely,

Daniyal Khan

March 6, 2026

WARTIME MONETARY AUSTERITY

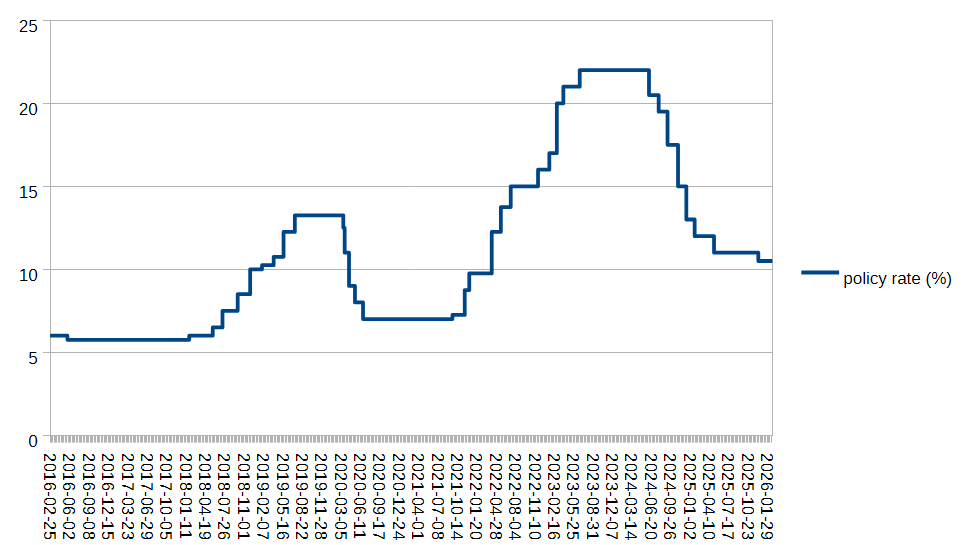

When I last wrote about monetary austerity (for the Monetary Policy Institute blog), the SBP had the policy rate almost at the peak of the post-Covid rate-hiking cycle. The monetary austerity regime has been dialed down, but remains painfully persistant. After a 50 bps reduction in the policy rate in December, the central bank’s monetary policy committee (MPC) chose not to change the rate on January 26. Business leaders were unhappy, again: according to the president of the Federation of Pakistan Chambers of Commerce and Industry (FPCCI), Arif Ikram Sheikh, businesses “had sought a reduction of 350 basis points to bring the policy rate to 7%, warning that high borrowing costs were exacerbating an already severe industrial crisis.”

Policy rate (Source:SBP)

But businesses can do nothing more than whimper and carry on licking their wounds. According to the SBP governor Jameel Ahmad, “Pakistan’s current phase of macroeconomic stabilisation is expected to hold for at least the next two years, … [and] the central bank will avoid unconventional or aggressive reductions in the policy rate.” That was before the war started. Businesses are now at the mercy of the MPC. When the policy rate fell by 50 bps in December, two of the nine MPC members had wanted only a 100 bps cut. When the policy rate was kept unchanged last month, three of the nine wanted a reduction of only 50 bps. This to me suggests a clearly conservative MPC composed of an even more conservative majority.

The central bank now has the 2026 calendar year’s second MPC meeting coming up on March 9. (The MPC meeting calendar for FY 2026 can be found here. There are two more meetings coming up in April and June.) The crucial factor in the decision will now be the war in the Middle East. Chances of a rate reduction were low anyway, but now I think the SBP is significantly less likely to reduce the policy rate. If anything, the policy rate might just go up. The aforementioned even-more-conservative majority on the MPC will likely prevail. The trouble is that a high interest rate is continuing to act as a cost side pressure on businesses. From here on out, a falling rate will not make up for fear-riddled markets dealing with prices which have remained high and an increase will only worsen the cost structure for businesses.

But the SBP, like other central banks, cannot help itself. There is a paucity of supply side measures. Economic orthodoxy contends that supply side measures like buffer stocks and inventories are not “efficient”, and thus must be shunned. And even if such measures are deployed, as they now might be, they are not in the hands of the central bank anyway. In a situation where there is an oil price shock and the closure of the Strait of Hormuz can cause all sort of problems for Pakistan, the absence of supply side measures is a real problem. (Gas to industry has already been cut.) (Voices from the oil sector are worried, and “reviving calls for the establishment of a strategic petroleum reserve (SPR) to manage emergencies.”) But as I said, the SBP can’t help itself. Yousuf Nazar, formerly of Citigroup, is absolutely correct that in saying that “[i]t will be a mistake for the central banks to raise interest rates if inflation spikes due to the rise in the energy prices” (@YousufNazar, Twitter, March 2, 2026). The central banks, including the SBP, I think, will do it anyway. They don’t and won’t know what else to do. When prices take a hit, central banks jump into action because it’s their mandate and they can’t not do it. On the one hand monetary orthodoxy dictates that letting high rates strangle the economy is prudence but on the other, refusing to raise rates is folly. Ultimately this is a reflection of modern central banks like the SBP not having any instruments in their arsenal to deal with supply side issues – and that there is something undoubtedly sadistic about monetary austerity.

The coming weeks will keep industry actors and policy makers nervous. While Israel is preparing for the war to continue “for several long weeks” and “the US campaign had been projected to last four to five weeks” according to Trump, Pakistan has about four weeks worth of fuel. The finance minister is now talking about how the government might manage fuel and energy consumption, including the possibility of closing higher education institutions. (There has also been some confusion about whether or not Pakistan’s airspace will be closed during March.) Nobody knows how long the war will last of course, but the prospect of a long drawn out war will surely be acknowledged as a real possibility all around. The bottom line is that the US and Israel’s attack on Iran and the resulting wider war could not have come at a worse time for anyone who was hoping that we might see an easing of monetary policy in Pakistan, however gradual and incremental. The MPC will now likely renew its faith in monetary austerity, pushed and pressured as it will feel by the dogs of war.

†